Friday, October 30, 2015

FINANCE & LAW TODAY: No addition for Gift from abroad if Donor gives st...

FINANCE & LAW TODAY: No addition for Gift from abroad if Donor gives st...: Case Law Citation:- CIT vs. Sudhir Budhraja (Delhi High Court), Income Tax (Appeal) no.59 of 2013, Date of Judgment: 13/10/2015 Brief ...

No addition for Gift from abroad if Donor gives statement before AO regarding his capacity despite non production of any document

Case Law Citation:- CIT vs. Sudhir Budhraja (Delhi High Court), Income Tax (Appeal) no.59 of 2013, Date of Judgment: 13/10/2015

Brief of the Case

Delhi High Court held In the case of CIT vs. Sudhir Budhraja that the findings of the Tribunal are based on sufficient material and cannot be stated to be perverse. On the other hand that the AO had no material or had not collected any evidence to reject the claim made by the Assessee. Apart from doubting and questioning the material produced by the Assessee, the AO had not produced any positive evidence which could lead to the inference that the amount received by the Assessee was not gift. High Court has has held that Insofar as the failure on the part of the donor to provide his business details, details of his assets, bank accounts and his agreements with his associates and other information is concerned; clearly, a donor could not be expected to share such details, which understandably may be considered as confidential.

Facts of the Case

The Assessee is a Chartered Accountant. The Assessee filed a return of income for the AY 1995-96 on 31st October, 1995 indicating gross professional receipts of Rs.18,95,901/- out of which Rs.18,05,400/- was received as consultancy fees from a US based company – M/s Blackfin Development Company Inc., USA (Blackfin). In addition the Assessee had also received US$ 6,00,000/- from Blackfin. It was the Assessee’s case that Blackfin had remitted the amount at the instance of Sh. Jaspal and it was a gift from him.

During the assessment proceedings on 3rd March, 1997, the donor appeared before the AO and was examined on oath. The donor affirmed that he and the Assessee had been close friends since 1971 and the remittance made was as a gift from him out of love and affection for the Assessee. He also stated that he had a business turnover of US$ 3-4 million. The Assessee was also examined on oath on 14th March, 1997 and 28th May, 1997. Thereafter, the Income Tax Authorities conducted a survey under Section 133A on the Assessee’s business premises and a questionnaire was issued to the donor. The donor replied the said questionnaire stating that he has already offered all explanations including his capacity and capability to make the gift and also the source of the gift. The Assessee was called upon to produce the agreement with Blackfin pursuant to which the Assessee had been engaged to provide consultancy services. The assessee produced the same

The AO passed an assessment order dated 27th March, 1998, inter alia, holding that although the entity of the donor had been established, the Assessee had failed to establish the capacity of the donor to make the gift or the genuineness of the transaction. The AO held that the Assessee had failed to substantiate his claim of having received the gift and added the amount of the aforesaid gift as income in the hands of the Assessee

Held by CIT (A)

CIT (A) rejected the appeal of assessee.

Held by ITAT

ITAT allowed the appeal of assessee. It was held that the Assessee had established the source of the gift as well as the creditworthiness of the donor, so accordingly addition is not allowed.

Held by High Court

The Tribunal held that the Assessee had discharged its burden as to the identity of the source as well as the capacity of the donor. The Tribunal’s findings are, essentially, findings of fact and there is little scope to interfere with the same unless it is concluded that the findings are perverse in law and/or are not based on any material. In CIT v. Sunita Vachani (1990) 184 ITR 121 (Del) this court held that ““in our opinion, the Tribunal had, on merits, come to the conclusion that the gifts were genuine. This is a pure question of fact. The Tribunal has examined the evidence which was available on the record and has arrived at the aforesaid finding. Even though it may be surprising as to how large sums of money are received by a family in India by way of gifts from strangers from abroad, unless there is something more tangible than suspicion, it will be difficult to regard the moneys received in India from abroad as representing the income of the assessee in India.”

There is no dispute that the identity of the donor has been established. The donor had appeared before the AO and recorded his statement on oath. He had affirmed (i) that he had gifted the amount in question to the Assessee out of love and affection; (ii) that the amount had been remitted by Blackfin at his instance; (iii) that he had known the Assessee since 1971 and was close to the Assessee; (iv) that his average annual income was 3-4 million dollars (equivalent to Rs.15 crores approximately); and the donor had also answered all other questions that were put to him.

Also the Assessee had recorded his statement affirming that he had received the gift from the donor. His statement also clearly indicated that he and the donor were friends since long and the donor was a highly successful businessman. The Assessee had also produced a copy of the notarised certificate issued by Blackfin confirming that the donor and Blackfin were associated since 1993 and the donor was to receive monies from Blackfin and that a sum of US$ 6,00,000/- had been remitted by Blackfin to the Assessee through its bank account on the instructions of the donor.

Insofar as the issue regarding discrepancy in the statement of the donor is concerned, we find that the same is not material in determining the question of the genuineness of the gifts or the capacity of the donor. it is apparent that the discrepancies in the statement are not significant. Insofar as the failure on the part of the donor to provide his business details, details of his assets, bank accounts and his agreements with his associates and other information is concerned; clearly, a donor could not be expected to share such details, which understandably may be considered as confidential.

The Assessee had produced the donor who answered all questions put to him. The Assessee as well as the donor had sworn statements indicating their close relationship going back several years. The Tribunal had concluded that the Assessee had discharged the burden. The AO on the other hand had not identified any material that was available with the Assessee, or should have been available with the Assessee, and had been withheld by him. In our opinion, the Tribunal rightly considered the issue in its correct perspective while holding that the Assessee had discharged his burden.

Insofar as the professional consultancy fee received from Blackfin is concerned, the Assessee had produced a copy of the agreement as well as the letter of termination. The agreement itself was in force for a period of six months and in terms of the agreement, the Assessee was to receive a sum of US$ 1,20,000 against, which the Assessee had received a sum of US$ 1,16,833. The Assessee had affirmed that except for the said arrangement it had no connection with Blackfin. The discrepancy in the amount received by the Assessee as consultancy fees and the amount receivable in terms of the agreement could not possibly be a ground for doubting the amount of gift as consultancy fees.

In Umacharan Shaw & Bros v. CIT: (1959) 37 ITR 271 (SC), the supreme court held that “ there was no material on which the Income-tax Officer could come to the conclusion that the firm was not genuine and further observed “the conclusion is the result of suspicion which cannot take the place of proof in these matters”. In the present case too, the AO had rejected the evidence produced and based his conclusion only on surmises; there was hardly any material for him to conclude that the amount in question was not a gift.

Accordingly, appeal of the revenue dismissed.

Regards

KK Singh

Prop - KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email - kksirclasses@hotmail.com, advocatekksingh@outlook.com

KK Singh

Prop - KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email - kksirclasses@hotmail.com, advocatekksingh@outlook.com

Thursday, October 29, 2015

FINANCE & LAW TODAY: ITAT empowered to allow deduction u/s 80IB (10) ev...

FINANCE & LAW TODAY: ITAT empowered to allow deduction u/s 80IB (10) ev...: Case Law Citation:- CIT vs. M/s Unitech Ltd. (Delhi High Court), Income tax (Appeal) no.239 of 2015, Date of Judgment: 05/10/2015 ...

ITAT empowered to allow deduction u/s 80IB (10) even if requirement u/s 80AC is not complied with, in case of conflict of opinions: HC

Case Law Citation:- CIT vs. M/s Unitech Ltd. (Delhi High Court), Income tax (Appeal) no.239 of 2015, Date of Judgment: 05/10/2015

Brief of the Case

Delhi High Court held In the case of CIT vs. M/s Unitech Ltd. that where there are conflicts of opinions of the various benches of the ITAT on the provision u/s 80AC of requirement of return filing before due date to claim deduction u/s 80IB (10), ITAT rightly allowed the deduction even the assessee filed his return of income after due date.

Facts of the Case

In the present case the Assessee filed its return of income for the on 2nd April 2009 claiming the benefit of deduction under Section 80IB (10). This was allowed by the AO while making assessment under Section 143(3) of the Income Tax on 30th December, 2009. In terms of Section 80AC of the Act the return had to be filed by the Assessee, ‘on or before the due date specified under Section 139(1) which in this case meant on or before 31st October, 2008.

Contention of the Assessee

The ld counsel of the assessee place reliance on the decisions of this Court in CIT v. Integrated Databases (I) Ltd. (2009) 178 Taxman 432 (Del) and CIT v. Contimeters Electricals (P) Ltd. (2009) 178 Taxman422 (Del).

He also placed reliance on the decision dated 26th June 2013 of the Andhra Pradesh High Court in ITTA No.114 of 2013 (CIT v. Sri S Venkataiah), the decisions dated 29th April 2013 of the ITAT Madras in ITA No.1214/Mds/2012 (ACIT vs. Precot Meridian Ltd.) and 4th February 2013 in ITA No. 1219-1223/Mds/2012 (ACIT v. V.N. Devadoss), the decisions of the ITAT Delhi dated 30th July 2010 in ACIT v. Dhir Global Industrial (P) Ltd. 133 TTJ (Del) 580 and dated 25th January 2012 in ITA No. 3352/Del/2011(Hansa Dalakoti v. ACIT), the decision of the Bangalore ITAT dated 12th April 2103 in M/s Vanshee Builders & Developers P. Ltd. v. CIT 63 SOT 30 and the decision of the Kolkata ITAT dated 19th April 2013 in ITA No. 1586/Kol/2012 (M/s Shelcon Properties (P) Ltd. v. JCIT).

Contention of the Revenue The ld counsel of the revenue placed reliance on the decision dated 27th August 2012 of the Uttarakhand High Court in ITA No. 07/2012 (Umesh Chandra Dalakoti v. Assistant Commissioner of Income Tax) as well as of the Calcutta High Court in CIT v. Shelcon Properties (P) Ltd. [2015] 370 ITR 305 (Cal) both of which have held the provision under Section 80AC of the Act to be mandatory.

Also he has referred to the decisions of the ITAT Special Bench in Saffire Garments v. ITO 20 ITR (Trib) 623, of the ITAT Madras Bench in 1219-1223/MDS/2012 (ACIT v. Shri V.N. Devadoss), of the ITAT Chandigarh Bench in 250-2511CHD/2003 (Lakshmi Energy and Food Ltd. v. ACIT) and the decision dated 30th January 2015 of the ITAT Mumbai Bench in ITA No. 4727/Mum/2012 (Dwarkadas Panchmatiya v. ACIT).

Held by ITAT

The ITAT while allowing appeal filed by the Assessee noted that there was a cleavage of opinion on the issue as was evident from two lines of decisions of the ITAT itself. Since a possible view in favour of the Assessee could be taken if one line of decisions was applied, the ITAT concluded that there was no justification for CIT to have invoked the jurisdiction Section 263 of the Act.

Held by High Court

In the case of CIT v. Sri S Venkataiah dated 26th June 2013 of the Andhra Pradesh High Court in ITTA No.114 of 2013, in which question was dealt with that whether the time limit for filing the return in terms of Section 80AC read with Section 139 (1) of the Act was mandatory. In this case, high court confirms the order of ITAT and held that Assessee appears to have shown “reasonable cause for filing the return of income belatedly” and that it was “beyond the control of the Assessee.”

On the other hand, the decisions of the Uttarakhand High Court in Umesh Chandra Dalakoti ITA No. 07/2012 dated 27th Aug. 2012 and of the Calcutta High Court in CIT v. Shelcon Properties (P) Ltd. [2015] 370 ITR 305 (Cal) appear to support the case of the Revenue that Section 80 AC is mandatory. There appears to be no authoritative pronouncement of this Court on the interpretation of Section 80AC of the Act and whether the said provision is mandatory or directory.

In the present case, there is no doubt that at the time of passing of order by CIT, there was a conflict of opinions of the various benches of the ITAT on whether 80AC was mandatory. Consequently, the ITAT was not in error in reversing the order of the CIT as far as the question of exercising jurisdiction under Section 263 was concerned.

It is clarified that the question whether the requirement under Section 80AC of the Act is mandatory is left open for consideration in an appropriate case.

Accordingly, appeal of the revenue dismissed.

Regards

KK Singh

Prop - KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email - kksirclasses@hotmail.com, advocatekksingh@outlook.com

KK Singh

Prop - KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email - kksirclasses@hotmail.com, advocatekksingh@outlook.com

Wednesday, October 28, 2015

FINANCE & LAW TODAY: All About Income Tax Advance Ruling Provisions

FINANCE & LAW TODAY: All About Income Tax Advance Ruling Provisions: A resident taxpayer may have some taxation issues in respect of a transaction which has been undertaken or proposed to be undertaken with...

All About Income Tax Advance Ruling Provisions

A resident taxpayer may have some taxation issues in respect of a transaction which has been undertaken or proposed to be undertaken with a non-resident. Similarly, a nonresident may have some taxation issues in respect of transaction which has been undertaken or proposed to be undertaken by him in India. In order to get clarification on taxation of those transactions, a person can make an application to the Authority for Advance Rulings („AAR‟). Provisions relating to advance ruling are provided in sections 245N to 245V.

In this part, you can gain knowledge about various provisions relating to advance ruling.

Meaning of advance ruling

Section 245N(a) gives the definition of „advance ruling‟. As per section 245N(a) “Advance Ruling” means :

- A determination by the AAR in relation to a transaction which has been undertaken or is proposed to be undertaken by a non-resident applicant.

- A determination by the AAR in relation to the tax liability of a non-resident arising out of a transaction which has been undertaken or is proposed to be undertaken by a resident applicant with such non-resident.

- A determination by the AAR in relation to the tax liability of a resident applicant, arising out of one or more transaction valuing Rs.100 crore or more [vide Notification No. 73/201 4, dated 28-11-2014] in total which has been undertaken or is proposed to be undertaken by such applicant and such determination shall include the determination of any question of law or of fact specified in the application.

- A determination or decision by the AAR in respect of an issue relating to computation of total income which is pending before any income-tax authority or the Appellate Tribunal. It shall include the determination or decision of any question of law or of fact relating to such computation of total income specified in the application.

- A determination or decision by the AAR\ whether an arrangement, which is proposed to be undertaken by any person being a resident or a non-resident, is an impermissible avoidance arrangement as referred to in Chapter X-A. [Chapter X-A contains provisions relating to General Anti-Avoidance Rule (GAAR)].

Meaning of Applicant

The application for advance ruling can be made by an applicant as defined in section 245N(b). As per section 245N an „applicant‟ would mean the following:

- A non-resident who has undertaken or proposes to undertake a transaction in India.

- A resident who has undertaken or proposes to undertake a transaction with a non-resident.

- A resident who has undertaken or propose to undertake one or more transactions of value of Rs.100 crore or more in total [vide Notification No. 73, dated 28-11- 2014]

- A resident falling within notified class or category of persons (presently includes public sector companies).

- Any person (resident or non-resident) making an application for determining whether an arrangement, is an impermissible avoidance agreement as referred to in Chapter X-A (applicable from 1-4-2015).

Applicant vis-a-vis the application

After understanding the meaning of “Advance Ruling” and “Applicant”, it is important to understand the nature of application which can be made by an applicant. Following Chart highlights the nature of application which can be made by various applicants:

| Nature of applicant | Nature of application |

| A non-resident applicant | A determination by the AAR in relation to a transaction which has been undertaken or is proposed to be undertaken by a non-resident applicant. Such determination shall include the determination of any question of law or of fact specified in the application. |

| A resident applicant who has undertaken a transaction with non-resident or proposes to undertake a transaction with non-resident. | A determination by the AAR in relation to the tax liability of a non-resident arising out of a transaction which has been undertaken or is proposed to be undertaken by a resident applicant with such non-resident. Such determination shall include the determination of any question of law or of fact specified in the application. |

| A resident who has undertaken or propose to undertake one or more transactions of value of Rs.100 crore or more in total; or | A determination by the AAR in relation to the tax liability of a resident applicant arising out of such transactions and such determination shall include the determination of any question of law or of fact specified in the application. |

| A resident falling within notified class or category of persons (i.e., a public sector company). | A determination or decision by the Authority in respect of an issue relating to computation of total income which is pending before any income-tax authority or the Appellate Tribunal and such determination or decision shall include the determination or decision of any question of law or of fact relating to such computation of total income specified in the application. |

| Any person (resident or non-resident) making an application for determination of whether an arrangement is an impermissible avoidance agreement as referred to in Chapter X-A. (applicable from 1-4-2015) | A determination or decision by the Authority whether an arrangement, which is proposed to be undertaken by any person being a resident or a non-resident, is an impermissible avoidance arrangement as referred to in Chapter X-A. (applicable from. 1-4-2015) |

Certain circumstances in which the application cannot be allowed

In following circumstances the application is not allowed by the AAR:

- when the question raised is already pending before any income-tax authority or appellate tribunal or any Court. However, exception will apply in the case of a resident applicant falling within the notified class or category of persons e. a public sector company.

- when the question involves determination of fair market value of any property.

- when the question relates to a transaction which is designed prima facie for the avoidance of income-tax. Exception to this provision: (i) resident taxpayer falling within notified class or category of persons e. a public sector company and (ii) Any person (i.e., resident or non-resident) making an application to determine whether an arrangement proposed to be undertaken is an impermissible avoidance arrangement under Chapter X-A.

Form of application

The application of advance ruling is to be made in the form prescribed in this regard. Different forms are prescribed for different applicants. Following Chart highlights the form of application applicable to different applicants.

| Applicant | Form of application |

| A non-resident applicant. | Form No. 34C (application should be in quadruplicate) |

| A resident seeking advance ruling in relation to a transaction undertaken or proposed to be undertaken by him with a non-resident. | Form No. 34D (application should be in quadruplicate) |

| A resident seeking advance ruling in relation to his tax liability arising out of one or more transactions valuing Rs. 100 crore or more in total which has been undertaken or proposed to be undertaken by him | Form No. 34DA (application should be in quadruplicate) |

| A resident falling within any such class or category of person as is notified by Central Government (i.e., a public sector company) | Form No. 34E (application should be in quadruplicate) |

| Any person (resident or non-resident) making an application for determination of whether an arrangement, is an impermissible avoidance agreement as referred to in Chapter X-A. (applicable from 1-4-2015) | Form No. 34EA (application should be in quadruplicate) |

Fees for filing the application

The fees payable along with application for advance ruling shall be in accordance with the following table:

| Category of applicant | Category of case | Fee |

| – A non-resident applicant.

– A resident seeking advance ruling in relation to the tax liability of a non-resident arising out of transaction undertaken or proposed to be undertaken by him with a non-resident.

– A resident seeking advance ruling in relation to his tax liability arising out of one or more transactions valuing Rs.100 crore or more in total which has been undertaken or is proposed to be

undertaken by him | Amount of one or more transaction, entered into or proposed to be undertaken, in respect of which ruling is sought does not exceed Rs. 100 crore. | Rs.2,00,000 |

| Amount of one or more transaction, entered into or proposed to be undertaken, in respect of which ruling is sought exceeds Rs. 100 core but does not exceed Rs. 300 crore. | Rs.5,00,000 | |

| Amount of one or more transaction, entered into or proposed to be undertaken, in respect of which ruling is sought exceeds Rs. 300 crore | Rs.10,00,000 | |

| Any other applicant | In all cases | Rs. 10,000 |

Documents to be submitted along with the application

- 4 copies of application in the prescribed form.

- Account-payee demand draft for the prescribed fees in favour of ‘Authority for Advance Ruling’s payable at New Delhi.

Person entitled to sign the application The application shall be signed by –

a) In the case of an individual –

- By the individual himself;

- Where, for any unavoidable reason, it is not possible for the individual to sign the application, the application can be signed by any person duly authorised by the individual in this behalf. However, in such a case, the person signing the application shall hold a valid power of attorney from the individual to do so, which shall be attached to the application.

b) In the case of a Hindu Undivided Family–

- By the karta thereof, and

- Where, for any unavoidable reason, it is not possible for the Karta to sign the application, by any other adult member of such family.

c) In the case of a company –

- by the Managing Director thereof, or where for any unavoidable reason such Managing Director is not able to sign and verify the application, or where there is no Managing Director, by any Director thereof;

- Where, for any unavoidable reason, it is not possible for the Managing Director or the Director to sign the application, by any person duly authorised by the company in this behalf. However, in such a case, the person signing the application shall hold a valid power of attorney from the company to do so, which shall be attached to the

d) In the case of a firm –

- by the managing partner of the firm.

- Where for any unavoidable reason such managing partner is not able to sign and verify the application or where there is no managing partner as such, by any partner of the firm other than a minor.

e) In case of an association of persons, the application should be signed by any member of the association or the principal officer thereof.

f) In case of any other person, the application should be signed by that person or by some person competent to act on his behalf.

Add Every application in the form as applicable shall be accompanied by the proof of payment of fees as specified in above table.

Can the application be withdrawn?

Application once made by the applicant can be withdrawn within a period of 30 days from the date of application.

Procedure on receipt of application for advance ruling

On receipt of an application, the AAR Shall send a copy thereof to the Principal Commissioner or Commissioner and, if necessary, will call upon him to furnish the relevant records. Where any records have been called for by the Authority in any case, such records shall, as soon as possible, be returned to the Principal Commissioner or Commissioner.

The Authority may, after examining the application and the records called for from the Commissioner, either allow or reject the application. The AAR shall not allow the application in certain circumstances (already discussed earlier). However, no application shall be rejected unless an opportunity has been given to the applicant of being heard. Where the application is rejected, reasons for such rejection shall be given in the order. A copy of every such order shall be sent, both to the applicant and to the Principal Commissioner or Commissioner.

Where an application is allowed, the AAR shall, after examining such further material as may be placed before it by the applicant or obtained by the AAR, pronounce its advance ruling on the question specified in the application.

On a request received from the applicant, the AAR shall, before pronouncing its advance ruling, provide an opportunity to the applicant of being heard, either in person or through a duly authorised representative(The term “Authorised representative” shall have the meaning assigned to it in section 288(2). )

The AAR shall pronounce its advance ruling in writing within six months of the receipt of application.

A copy of the advance ruling pronounced by the AAR, duly signed by the Members and certified in the prescribed manner shall be sent to the applicant and to the Principal Commissioner or Commissioner, as soon as possible, after such pronouncement.

Restriction on further procedure

No income-tax authority or the Appellate Tribunal shall proceed to decide any issue in respect to which an application has been made to the AAR by an applicant, being a resident.

Applicability of advance ruling

The advance ruling pronounced by the AAR shall be binding only on the applicant who had sought it and that too in respect of the transaction in relation to which the ruling had been sought. Further, it shall be binding on the Principal Commissioner or Commissioner and the Income-tax authorities subordinate to him, in respect of the applicant and the said transaction.

The advance ruling pronouncement as stated above shall be binding as aforesaid, unless there is a change, in law, or facts on the basis of which the advance ruling was pronounced.

Advance ruling to be void in certain circumstances.

Where the AAR finds, on a representation made to it by the Principal Commissioner or Commissioner or otherwise, that an advance ruling pronounced by it has been obtained by the applicant by fraud or misrepresentation of facts, then the Authority may, by an order, declare such ruling to be void ab initio and thereupon all the provisions of the Act shall apply to the applicant as if such advance ruling had never been made.

A copy of the order made as above shall be sent to the applicant and to the Principal Commissioner or Commissioner.

Powers of the AAR

The AAR shall, for the purpose of exercising its powers, have all the powers of a civil court under the Code of Civil Procedure, 1908 as are referred to in section 131 of this Act. Powers vested under section 131 are discovery and inspection, enforcing the attendance of any person, including any officer of a banking company and examining him on oath, compelling the production of books of account and other documents, and issuing commissions. It will also have the power to regulate its own proceeding in all the matters arising out of the exercise of its powers under the Income-tax Act.

The AAR shall be deemed to be a civil court for the purposes of section 195 but not for the purposes of Chapter XXVI of the Code of Criminal Procedure, 1973 and every proceeding before the Authority shall be deemed to be a judicial proceeding under certain provisions of the Indian Penal Code.

Regards

KK Singh

Prop - KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email - kksirclasses@hotmail.com, advocatekksingh@outlook.com

Tuesday, October 27, 2015

FINANCE & LAW TODAY: All about Rectification of Mistake under Section 1...

FINANCE & LAW TODAY: All about Rectification of Mistake under Section 1...: Introduction Sometimes there may be a mistake in any order passed by the Assessing Officer. In such a situation, mistake which is appar...

All about Rectification of Mistake under Section 154

Introduction

Sometimes there may be a mistake in any order passed by the Assessing Officer. In such a situation, mistake which is apparent from the record can be rectified under section 154. This article discusses provisions relating to rectification of mistake under section 154 of Income Tax Act, 1961.

Order which can be rectified under section 154

With a view to rectifying any mistake apparent from the record, an income-tax authority may, –

- Amend any order passed under any provisions of the Income-tax Act.

- Amend any intimation or deemed intimation sent under section 143(1).

- Amend any intimation sent under section 200A(1)(*) [section 200A deals with processing of statements of tax deducted at source i.e. TDS return].

- amend any intimation under section 206CB*.

(*) Under section 200A, a TDS statement is processed after making correction of any arithmetical error in the statement or after correcting an incorrect claim, apparent from any information in the statement

Similarly a new section 206CB is inserted by Finance Act, 2015 to provide for the processing of TCS statement.

If due to rectification of mistake, the tax liability of the taxpayer is enhanced or refund is reduced, the taxpayer shall be given an opportunity of being heard.

Rectification of order which is subject to appeal or revision

If an order is the subject-matter of any appeal or revision, any matter which is decided in such an appeal or revision cannot be rectified by the Assessing Officer. In other words, if an order is subject matter of any appeal, then the Assessing Officer can rectify only those matters which are not decided in such appeal.

Initiation of rectification by whomThe income-tax authority can rectify the mistake on its own motion.

The taxpayer can intimate the mistake to the income-tax authority by making an application to rectify the mistake.

If the order is passed by the Commissioner (Appeals), then the Commissioner (Appeals) can rectify mistake which has been brought to notice by the Assessing Officer or by the taxpayer.

Time-limit for rectification

No order of rectification can be passed after the expiry of 4 years from the end of the financial year in which order sought to be rectified was passed. The period of 4 years is from the date of order sought to be rectified and not 4 years from original order. Hence, if an order is revised, set aside, etc., then the period of 4 years will be counted from the date of such fresh order and not from the date of original order.

In case an application for rectification is made by the taxpayer, the authority shall amend the order or refuse to allow the claim within 6 months from the end of the month in which the application is received by the authority.

The procedure to be followed for making an application of rectification

Before making any rectification application the taxpayer should keep following points in mind.

- The taxpayer should carefully study the order against which he wants to file the application for rectification.

- Many times the taxpayer may feel that there is any mistake in the order passed by the Income-tax Department but actually the taxpayer’s calculations could be incorrect and the CPC might have corrected these mistakes, e.g., the taxpayer may have computed incorrect interest in return of income and in the intimation the interest might have been computed correctly.

- Hence, to avoid application of rectification in above discussed cases the taxpayer should study the order and should confirm the existence of mistake in the intimation, if any.

- If he observes any mistake in the order then only he should proceed for making an application for rectification under section 154.

- Further, he should confirm that the mistake is one which is apparent from the records and it is not a mistake which requires debate, elaboration, investigation, The taxpayer can file an online application for rectification of mistake.

- For rectification of intimation under Section 200A(1)/206CB online correction statement is to be filed;

- An amendment or rectification which has the effect of enhancing the assessment or reducing a refund or otherwise increasing the liability of the taxpayer (or deductor) shall not be made unless the authority concerned has given notice to the taxpayer or the deductor of its intention to do so and allowed the taxpayer (or the deductor) a reasonable opportunity of being heard.

Extract of Section 154 of Income Tax Act, 1961

Rectification of mistake.

154. (1) With a view to rectifying any mistake apparent from the record an income-tax authority referred to in section 116 may,—

(a) amend any order passed by it under the provisions of this Act ;

(b) amend any intimation or deemed intimation under sub-section (1) of section 143;

(c) amend any intimation under sub-section (1) of section 200A;

[(d) amend any intimation under sub-section (1) of section 206CB.]

(1A) Where any matter has been considered and decided in any proceeding by way of appeal or revision relating to an order referred to in sub-section (1), the authority passing such order may, notwithstanding anything contained in any law for the time being in force, amend the order under that sub-section in relation to any matter other than the matter which has been so considered and decided.

(2) Subject to the other provisions of this section, the authority concerned—

(a) may make an amendment under sub-section (1) of its own motion, and

(b) shall make such amendment for rectifying any such mistake which has been brought to its notice by the assessee or by the deductor or by the collector, and where the authority concerned is the Commissioner (Appeals), by the Assessing Officer also.

(3) An amendment, which has the effect of enhancing an assessment or reducing a refund or otherwise increasing the liability of the assessee or the deductor or the collector, shall not be made under this section unless the authority concerned has given notice to the assessee or the deductor or the collector of its intention so to do and has allowed the assessee or the deductor or the collector a reasonable opportunity of being heard.

(4) Where an amendment is made under this section, an order shall be passed in writing by the income-tax authority concerned.

(5) Where any such amendment has the effect of reducing the assessment or otherwise reducing the liability of the assessee or the deductor or the collector, the Assessing Officer shall make any refund which may be due to such assessee or the deductor or the collector.

(6) Where any such amendment has the effect of enhancing the assessment or reducing a refund already made or otherwise increasing the liability of the assessee or the deductor or the collector, the Assessing Officer shall serve on the assessee or the deductor or the collector, as the case may be a notice of demand in the prescribed form specifying the sum payable, and such notice of demand shall be deemed to be issued under section 156 and the provisions of this Act shall apply accordingly.

(7) Save as otherwise provided in section 155 or sub-section (4) of section 186 no amendment under this section shall be made after the expiry of four years from the end of the financial year in which the order sought to be amended was passed.

(8) Without prejudice to the provisions of sub-section (7), where an application for amendment under this section is made by the assessee or by the deductor or by the collector on or after the 1st day of June, 2001 to an income-tax authority referred to in sub-section (1), the authority shall pass an order, within a period of six months from the end of the month in which the application is received by it,—

(a) making the amendment; or

(b) refusing to allow the claim.

Regards

KK Singh

Prop - KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email - kksirclasses@hotmail.com, advocatekksingh@outlook.com

Monday, October 26, 2015

FINANCE & LAW TODAY: Changes in Form No.15G and 15H & related procedure...

FINANCE & LAW TODAY: Changes in Form No.15G and 15H & related procedure...: Tax payers seeking non-deduction of tax from certain incomes are required to file a self declaration in Form No. 15G or Form No.15H as pe...

Changes in Form No.15G and 15H & related procedures wef 01.10.2015

Tax payers seeking non-deduction of tax from certain incomes are required to file a self declaration in Form No. 15G or Form No.15H as per the provisions of Section 197A of the Income-tax Act, 1961 In order to reduce the cost of compliance and ease the compliance burden for both, the tax payer and the tax deductor, the Central Board of Direct Taxes (CBDT) has simplified the format for self declaration in Form No.15G or 15H. The procedure for submission of the Forms by the deductor has also been simplified in the Income-tax Rules, 1962 by substituting newly constructed rule 29C.

Under the simplified procedure, a payee can submit the self-declaration either in paper form or electronically. The deductor will not deduct tax and will allot a Unique Identification Number (UIN) to all self-declarations in accordance with a well laid down procedure to be specified separately. The particulars of self-declarations will have to be furnished by the deductor along with UIN in the Quarterly TDS statements. The requirement of submitting physical copy of Form 15G and 15H by the deductor to the income-tax authorities has been dispensed with. The deductor will, however be required to retain Form No.15G and 15H for seven years. These changes will come into force on the 1st day of October, 2015 as per the Notification issued vide S.O. No.2663 (E) dated 29th September 2015. This is a welcome decision for honest tax payers but a cautioning alarm for habitual violators. It is felt that it is more revenue oriented and is more beneficial for the income tax department than that of the tax payers

Advatnages and features:

1. Proper adherence:

The deductor has to check whether person providing the form is eligible to submit requisite form or not and that too according to particulars submitted by the person. Thus there is more responsibility on the deductor now than was in the past, who now has to ensure that the person submitting these forms is in-fact eligible to submit either form 15G or 15H. The eligibility will be measured on two counts. One pertains to the age of the deductee and the other pertains to the non taxable portion of income. The decutor can ensure former on the basis of DOB on PAN card or Adhar card or KYC documents available with them whereas latter condition of Income can be verified on the basis of the estimate of the customer. The banker can not ordinarily dispute income of the customer and has to accept it as it is. However, if the income received by the customer is known to the bankers being paid by them, then they can not escape from the liabilities if they accept the incorrect figures in form and latter on taxpayer defaults.

2. Proper information:

The deductor has to ensure that the person submitting the form has stated correct PAN in the form 1 5G or 1 5H and the same is properly verified by the deductor and the PAN is saved in its record for future reference. If the form contains defective or no mention of PAN, then tax will have to be deducted at 20%. This will ensure discipline in compliance as both deductor and deductee will be under an obligation to provide correct details to the income tax department. The bankers in the past were considering this ‘process’ as a ritual without any responsibility and now in future they will be under scanner of the department for receiving these forms for incomplete/defective details

3. Physical as well as electronic submission:

Eligible deductee may now file form 15G/15H in paper form physically or submit the said form electronically after deductor like banks and others make necessary arrangements to provide such facility on their online websites. These customers may submit Form 15G /Form 15H by using the website of the banks. On receipt of this form, the deductor will not deduct tax and will allot a Unique Identification Number (UIN) to all self-declarations. It is to be noted that UIN should be separate for each type of form and quarter.

4. Electronic compliances with less paper work:

The particulars of self-declarations made by the customers either through form 15G or 15H will have to be furnished by the deductor along with UIN in the Quarterly TDS statements of the deductor. The forms received in a particular quarter are required to be reported in quarterly etds return even if there is no deduction in that quarter. The requirement of submitting physical copy of Form 15G and 15H by the deductor to the income-tax authorities has been dispensed with. The department then will specify this information in 26AS of the concerned customer for verification and knowledge of the assessing officer. Deductor is required to retain the form 15G/15H for seven years.

5. Only resident can file

Form No 15G or 15H can be filed only by residents. NRI can not fie this form. In form 15G /15H person has to provide details of Income for which form 15G/15H has been submitted.

6. Why, who and when this form needs to be submitted

Getting a tax refund can be cumbersome for few as delays by the Income Tax Department are common. It makes sense to plan your taxes at the beginning of the year, to avoid over payment and the refund process. Submitting investment declaration with your employer on time and filling form 15G/15H will save your half the hassles. However, you cannot randomly submit forms 15G and 15H. There are certain precautions one should take while submitting these forms. Filing a wrong form without being eligible to do so would be illegal and could involve payment of interest on the tax payable and also attracts penal consequences. If your interest income exceeds 10,000 a year, the bank will deduct 10% tax at source. If you do not furnish PAN details, the TDS rate will be higher at 20%. However, you can submit a Form 15G and 15H to avoid TDS on interest income subject to satisfaction of conditions.

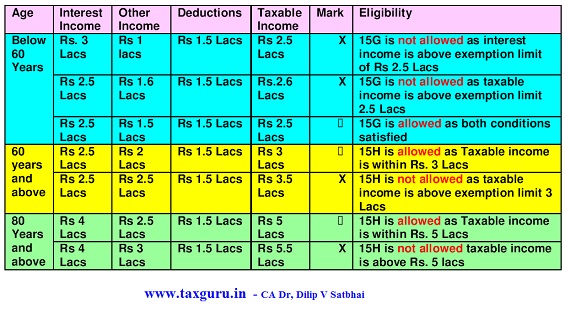

a) Who can submit form No. 15G?

A person (Individual, HUF) who is resident in India can submit form No. 15G. NRI cannot submit this form. The Person below sixty years needs to fulfill the following two conditions to become eligible to submit Form 15G,:

i) The estimated total income computed as per the provisions of the Income Tax Act is less than or equal to basic exemption limit i.e. Rs. 2,50;000 for the AY 201 5-16 and onwards and

ii ) The aggregate amount of interest income etc. received during the financial year should not exceed the basic exemption limit i.e Rs 2,50,000 for the AY 2015-16 and onwards.

If both these conditions are satisfied, Form 15G may be submitted to the deductor and entire interest income could be received without any deduction of tax at source.

b) Who can submit form No. 15H?

Any resident individual, who is of the age of sixty years or above can submit form No. 15H provided his estimated income is less than or equal to basic exemption limit i.e Rs. 3,00,000 for the AY 201 5-16 onwards. This form can be submitted only by the senior citizen even though the total interest amount from the payer may exceed Rs. 3,00,000 (i.e., the limit of basic exemption limit).

The following table will explain the concept of eligibility to furnish Form 15G and 15H

c) Penalty for incorrect/wrong submission of Form 15G or 15F

Imprisonment and fines await those who wrongly file the two forms to avoid tax on interest income liable for tax deduction at source.

• False statement in verification or delivery of false account, etc.

Section 277 provides for prosecution for making false statement or producing false accounts /documents. If a taxpayer makes statement in any verification under the Act or under any rules made thereunder, or delivers an account or statement which is false, and [As amended by Finance Act, 2015] which he either knows or believes to be false, or does not believe it to be true, he shall be punishable as follows:

i)With rigorous imprisonment which shall not be less than 6 months but which may extend to seven years and with fine where tax sought to be evaded exceeds Rs. 25 lakh (Rs. 1 lakh upto 30-6-2012).

ii) With rigorous imprisonment which shall not be less than 3 months but which may extend to two years (3 years upto 30-6-2012) and with fine in other cases.

- Failure to comply with provisions of relating to Permanent Account Number (PAN)

Section 272B provides penalty in case of default by the taxpayer in complying with the provisions of section 139A or knowingly quoting incorrect PAN in any document referred to in section 139A(5)(c) or intimates incorrect PAN for the purpose of section 1 39A(5A)/(5C). Penalty under section 272B is Rs. 10,000.

Regards

KK Singh

Prop - KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email - kksirclasses@hotmail.com, advocatekksingh@outlook.com

Subscribe to:

Comments (Atom)