Saturday, November 28, 2015

FINANCE & LAW TODAY: Speculative loss can be carried forward even if re...

FINANCE & LAW TODAY: Speculative loss can be carried forward even if re...: Citation of the case:- ITO Vs Ramesh Kumar Jajodia(ITAT Kolkatta),ITA No.2166/Kol/2013, Date of decision: 07-10-2015. Brief of the cas...

Speculative loss can be carried forward even if revised return claiming loss is filed u/s 139(5)

Citation of the case:- ITO Vs Ramesh Kumar Jajodia(ITAT Kolkatta),ITA No.2166/Kol/2013, Date of decision: 07-10-2015.

Brief of the case:

ITAT held in ITO Vs Ramesh Kumar Jajodia that if the assessee had filed its original return u/s 139(1) but forgot to claim the speculative loss in its original return and filed revised return u/s 139(5) and claimed the loss in its revised return then the speculative loss should be allowed to be carried forward.

Moreover if there was clerical mistake in filling up the ITR form then then the assessee should not be deprived of the benefit of carrying forward of loss. As per provision of section 139(9), where a return furnished by the assessee was considered defective, the assessing officer may intimate the defect to the assessee giving him opportunity to remove the same within fifteen days or further time allowed. So AO should have given the assesse opportunity to rectify its return.

Facts of the case:

The assessee had filed its return of income before due date mentioned u/s 139(1) but forgot to claim the speculative loss so it filed revised return within the date mentioned u/s 139(5) and also carried forward the speculative loss but AO disallowed the same on the plea that loss could only be carried forward only if the return was filed u/s 139(1) and loss was claimed under that return and in the above case loss was claimed in the return filed u/s 139(5) so loss could not be allowed to be carried forward.

Contention of the assessee:

Assessee was of the view that clerical/typographical mistake in filling of columns while filing the return should not deprive the appellant benefit of carrying forward a loss for which he was otherwise entitled. At most it could be said that the columns of the return have not been filled in properly. As per provision of section 139(9), where a return furnished by the assessee was considered to be defective, the assessing officer may intimate the defect to the assessee giving him opportunity to remove the same within fifteen days or further time allowed. Clause (a) to the explanation to the said sub-section clarifies that unless necessary statements and columns in the return have been duly fill in, the return can be treated as defective. Therefore, this was the case of defective return and the AO should have been given opportunity to remove the defect by filling in the relevant schedules in a correct manner. AO directly disallowed the claim of loss so AO should be directed to give the assessee opportunity of being heard

Contention of the revenue:

Revenue was of the view that as per the provisions of income tax, loss could only be carried forward if the original return was filed u/s 139(1) and the loss was claimed in that return but as the assessee had claimed the speculative loss by filing the revised return u/s 139(5) so loss should not be allowed to be carried forward as it was against the provisions of income tax act.

Held by ITAT:

ITAT held that as the return was filed by the assessee u/s 139(1) The assessee revised the return finally within the time allowed u/s. 139(5) of the Act. Even otherwise, this disallowance off loss claimed in speculative transactions u/s. 143(5) of the Act cannot be disallowed by acting u/s 143(1) of the Act. Because this is a highly debatable issue and debatable issue cannot be adjudicated while passing intimation u/s. 143(1) of the Act.

So appeal of the revenue was dismissed.

Regards

KK Singh

Prop-KK Sir's Classes

wwwkksingh.blogspot.in

wwwkksir.blogspot.in

Email- kksirclasses@hotmail.com,advocatekksingh@outlook.com

Monday, November 23, 2015

FINANCE & LAW TODAY: Peer to Peer (P2P) Lending: Business Models

FINANCE & LAW TODAY: Peer to Peer (P2P) Lending: Business Models: Rise of P2P Business With the advancement in technology, there has been a dramatic change in the lifestyle and perception of people, fro...

Peer to Peer (P2P) Lending: Business Models

Rise of P2P Business

With the advancement in technology, there has been a dramatic change in the lifestyle and perception of people, from sharing their mood on facebook or becoming an overnight celebrity by trolling on Instagram or twitter to crowd funding from across globe for a social cause, to starting a business idea online. Technology has opened a virtual world which is now gaining traction for doing business surpassing geographical limitations. With the emergence of new and improved technologies, lives have become much more easier (if we could say so) than what it was just a decade back.

In the era where everybody is connected to the world wide web, there is much happening on exploring financial intermediation through technology as well. Lending and borrowing is an age old relationship. Right from the days of usurious money lending to intermediation by banks and financial institutions. Technology is now ushering an era of removing the limitations of physical presence for lending decisions and is buzzing to create a new virtual space for undertaking lending decisions. An outcome of this is emergence of a business model called, peer to peer lending, more popularly known as P2P lending[1].

P2P is a process where the lenders and the borrowers come together on a virtual platform in a bid to undertake financial business. The role of the platform is limited to acting as a facilitating agent, in some more complex models P2P platform is actively engaged in lending apart from acting as facilitation centre.

The focus of the article is to understand the current models of P2P lending across the globe.

Current Scenario of P2P Business

Peer to Peer Lending has become an important part of the financial services sector in many countries worldwide. Companies like Lending Club, in the United States of America and Zopa in the United Kingdom[2], which started their operation just few years back have already became a threat to the retail banks. These companies are now worth billions. They advance loans of nearly equal values as any retail banks in the respective countries.

The key factor that has led to success of these companies is, that instead of advancing loans to borrowers out of their own fund they tend to bring together the members of common public of a country who have idle funds and the ones who are in need of funds. These companies acts as intermediaries between the lender and borrowers. By acting as intermediary they avoid the traditional risk which a bank has to face as they act as borrower to every lender and lender to every borrower.

There are numerous success stories of P2P lending companies (company) worldwide[3], but this must be noted that business of rolling 3rd party money isn’t the easiest one to clone and achieve success as it depends on multiple factors including regulatory framework, public’s mind-set toward credit and taking up risk, structure and diversity of the economy, etc.

With the emergence of new technologies and cheaper cost of communications P2P lending companies tend to have much wider reach than the banks. The transacting parties do not need to come together physically, instead they come together to transact on virtual platforms set up by these P2P lending companies. By use of these platform people are able to raise funds and disburse loans from distant or remote locations, just by logging on to the virtual platforms provided by the P2P lending companies.

There are two models that are prevalent globally,

a) client-segregated account model; and

b) notary model.

The modus operandi of the two models is illustrated below.

Types of P2P model[4]

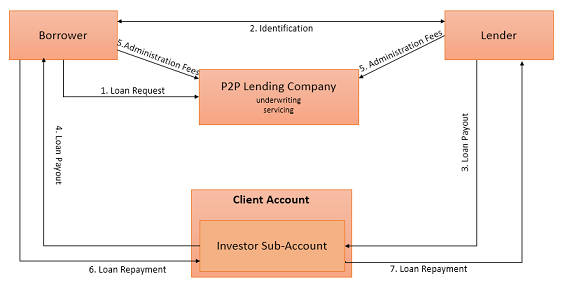

1. CLIENT-SEGREGATED ACCOUNT MODEL.

This is the simplest form of P2P model, where the lenders directly interact with the borrowers and they themselves fix their counter parties.

The process of client-segregated accounts model is briefed below:

- The borrower first put in their loan request on the P2P site,

- These loan requests are then listed on the P2P website for the lenders to identify and act on the loan requests.

- After successful identification and assessment of credit worthiness and various other factors related to the borrower, the lenders then release the funds in favour of the borrowers, which are deposited into a specific account called the Investor Sub-Account maintained with the P2P company, there a separate investor sub-account for each and every client (lender and borrower).

- These funds are then transferred into the Investor Sub-Account of the borrower for him to withdraw the same as per his convenience.

- After the funds reach the borrower the P2P company charge their administration fee from both of the clients.

- At time of repayment (both principle and interest) the borrower deposit the amount in the same Investor Sub-Account.

- These funds are then transferred to the lender’s accounts, which are then available for the lender to withdraw or use them to fund further transactions at the P2P portal.

This form of P2P model is very transparent as both the parties have complete knowledge of where their hard earned money is going or to whom one needs to pay, to pay off ones debts. Here the lenders do not face any risk of losing their money in the event of bankruptcy of the P2P company as there is a direct agreement between the lender and the borrower, nor the company faces any risk of claims from the lenders in case of default of the borrowers, as the lenders are the sole decision makers based on their own discretion, whether to advance a loan to a specific borrower or not.

2. NOTARY MODEL

This is is a much complex form of P2P business, which involves a commercial bank apart from the lender or the borrower.

The process of the notary model is briefed below:

- The borrower first put in their loan request on the P2P site.

- The P2P company then forward the loan request to a commercial bank associated with the company, the bank then sanction the loan and issue a loan promissory note to the company.

- The company then forward the promissory note to the borrower.

- The company then charges its admonition fees form the borrower.

- The borrower then submits the promissory note to the issuing bank.

- The bank in return pays the promised loan amount to the borrower.

- Meanwhile the company lists the loan request on its website, for the lenders to view them and advance funds to finance the loan request.

- Ones there is sufficient funds with the company from the lenders, the company immediately buys the loan receivables form the commercial bank. And issues pass through certificates (ptc) to lenders in proportion to their fund in a single loan.

- At this time the company charges its administration fees from the lenders.

- At time of repayment of the loans, the borrowers pay the company to pay off their debts.

- Which are passed to the lenders accounts held with the company for funding further loan transaction or withdrawal by the lenders.

This form of P2P model is advantageous to the borrowers as they do not need to wait for a lender to identify him/her and advance them loans, instead the company helps the borrowers by making the loans originate from the bank as soon as possible and later converting the loan into a P2P loan. This is the model used by the industry leaders like Lending Club and Zopa.

Impact of P2P business

P2P lending is growing fast worldwide and if it keeps the same pace of growth it is set to overtake the traditional system of banking in the next decade.

In the United States the amount of loan disbursed by Lending club alone upto the year 2014 is over US$ 8 billion[5], which is very low as compared to the total of the country’s retail deposits, but for a player who entered the market just 7 years back, the amount of loan disbursed by it is huge.

In the United Kingdom, the value of total loans disbursed by the P2PL companies raised from £ 871 million in 2012 to £ 2.4 billion in 2013, and since then the amount kept doubling every 6 month – 1 Year. Though this is a very small amount as compared to the €1.2 trillion retail deposits of the country, the rate of their growth is surely seen as a threat by the commercial banks of the country.

Though the concept of P2P lending originated in the UK and was developed in the USA, China the 2nd largest economy of the world is not lacking behind in any aspect in exploiting the advantages of P2P lending. Ppdai was the first P2P lending to go live in China in June 2007 and since then the no of P2P companies has been on a constant rise. Due to the conservative policies of China no one knows of the total revenues of these platforms, but they surely are making some decent profits to continue to remain in business and even attract new entrants, who are not only from within China but from overseas as well. Alibaba Group Holdings Ltd’s[6] finance arm is all set to create a P2P market place worth US$ 163 billion (¥ 1 trillion) in China by the year 2016, it launched its P2P platform “Zhao Cai Bao” in April, 2015 and is already a market place worth ¥ 14 billion. The CEO of Zhao Cai Bao stated – “Think of us as an exchange for loans”. It can be clearly understood from these words that Zhao Cai Bao is openly challenging the retails banks of China in their lending business.

These countries even have strict regulations to keep check on the amounts of money circulated by these platforms, as they deal with public money they are needed to comply with strict regulations to protect the general public of the country

In USA the Securities Exchange Commission regulates the P2P lending companies, in UK the P2PL companies are regulated by the Financial Authority and in China they are regulated by the People’s Bank of China, which is even the central bank of the country.

Conclusion: P2P lending scenario in India

While the entire world is seeing a boom in P2P funding, in India the P2P lending is still not prevalent and has no recognition at all. Even more, there are no regulation governing P2P lending. While the common laws of the country are largely based on the UK common laws and are largely facilitating and broad based in nature, the regulatory complexity and unclarity on P2P model has acted as a major deterrent in venturing into the region. There is ambiguity on whether P2P would be seen as crowd funding model or will be seen as a collective investment scheme. The Securities Exchange Board of India (SEBI)[7] has a draft on crowd funding but there is still a long way to go before the same is finalised and implemented. Lack of understanding on the regulatory side is one of the primary causes that P2P has not taken off in India. see our article on legal aspects of p2p in India – http://www.moneylife.in/article/is-peer-to-peer-lending-too-futuristic-in-india/43545.html.

The slow or late emergence of P2P lending in India is mainly due to the mind-set of the people, who do not want to take risk of advancing loans in order to earn higher on their idle funds and still prefer the traditions system of approaching the banks for deposits and investments. India needs to catch fast with the rest of the world in this regard to enjoy the early benefits from this new system.

Regards

KK Singh

Prop- KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email- kksirclasses@hotmail.com,advocatekksingh@outlook.com

Sunday, November 22, 2015

FINANCE & LAW TODAY: Govt may bring down Corporate Tax from 30% to 25%

FINANCE & LAW TODAY: Govt may bring down Corporate Tax from 30% to 25%: Press Information Bureau Government of India Ministry of Finance 20-November-2015 Government Calls for Comments on Proposed Plan of Phas...

Govt may bring down Corporate Tax from 30% to 25%

Press Information Bureau

Government of India

Ministry of Finance

20-November-2015

Government of India

Ministry of Finance

20-November-2015

Government Calls for Comments on Proposed Plan of Phasing-Out Exemptions and Deductions under the Income-Tax Act in Order to Bring Down Rate of Corporate Tax from 30% to 25%

The Union Finance Minister Shri Arun Jaitley in his Budget Speech 2015 had indicated that the rate of Corporate Tax will be reduced from 30% to 25% over the next four years along with corresponding phasing-out of exemptions and deductions. This is a step towards simplification of tax laws, which is expected to bring about transparency and clarity.

The Government proposes to implement this decision in the following manner:

- Profit linked, investment linked and area based deductions will be phased out for both corporate and non-corporate tax payers.

- The provisions having a sunset date will not be modified to advance the sunset date. Similarly the sunset dates provided in the Act will not be extended.

- In case of tax incentives with no terminal date, a sunset date of 31.3.2017 will be provided either for commencement of the activity or for claim of benefit depending upon the structure of the relevant provisions of the Act.

- There will be no weighted deduction with effect from 01. 04.2017.

The details of proposed phasing-out of deductions are available on the website of the Income Tax Department at www.incometaxindia.gov.in.

Comments on this proposal may be sent within 15 days to Director (TPL-III) on mail at dirtpl3@nic.in or by post at Director (TPL III), Central Board of Direct Taxes, Room No. 147G, North Block, New Delhi- 110001.

Regards

KK Singh

Prop-- KK Sir's Classes

wwwkksir.blogspot.in

wwwkksir.blogspot.in

Email- kksirclasses@hotmail.com,advocatekksingh@outlook.com

Friday, November 20, 2015

FINANCE & LAW TODAY: Attachment of Bank Account pending stay petition –...

FINANCE & LAW TODAY: Attachment of Bank Account pending stay petition –...: 1. VAT authorities in various States resort to attachment of bank accounts of dealers in a routine manner, totally ignoring the judicial ...

Attachment of Bank Account pending stay petition – Need for instructions to VAT Authorities

1. VAT authorities in various States resort to attachment of bank accounts of dealers in a routine manner, totally ignoring the judicial precedents on the subject and against the principles of natural justice.

2. Many a time, bank accounts are attached while stay petition filed by the dealer is pending before the appellate authority. Attachment notice is sent to the bank along with notice to the dealer to deposit pending disputed dues, without giving any opportunity to the dealer to represent his case. In some of the cases, attachment notices are sent to the bank simultaneously along with assessment orders, even before expiry of time allowed for filing appeal and stay petitions, in gross violation of the legal provisions.

3. Attachment of bank accounts disrupt the business operations of the dealers and therefore they would have no other option but to move jurisdictional high courts to get the attachment notices vacated, which involves huge expenditure and waste of time which could have been otherwise used for business purposes.

4. High Courts have time and again granted relief to the dealers, by vacating the attachment notices and directing the appellate authorities to dispose the stay petitions on priority. But, pity is VAT departments continue to resort to attachment of bank accounts of dealers, ignoring the directions of the High Courts, on flimsy ground that the relief given by High Court in a particular case does not applicable to other assesses.

5. In the recent case of Automark Industries (I) Ltd. Vs. State of Gujarat, the High Court of Gujarat vide its order Dt.17.10.2015 vacated the attachment notices issued by the department and directed the Dy. Commissioner (Appe als) to decide the stay petitions filed by the dealers within 15 days. In this case the department has served attachment notices on three banks for the same amount of disputed demand. Had there been balance in three banks, the money would have been transferred by banks to Government account resulting in recovery of thrice the amount of disputed demands. The High Court held that “When the petitioner had already preferred an appeal with a stay application, the least that was expected of the fourth respondent was to wait for the outcome of the stay application before resorting to coercive measures as has been done in the present case. Besides, the orders u/s 44 also suffer from the vice of non-application of mind, inasmuch as, in the notices issued to each of the banks, the fourth respondent has sought to recover the entire demand covered under the notice from each of the banks. As rightly submitted by the counsel for the petitioner, in case there were sufficient funds in each of the bank accounts, the fourth respondent would have succeeded in recovering thrice the amount covered under the demand notice. When drastic powers are conferred on the executive, it is imperative that those powers be exercised with due sense of responsibility and with circumspection by an officer or authority. While the fourth respondent is vested with drastic powers u/s 44, it is expected that such powers are exercised in a reasonable manner and not arbitrarily, as has been done in the present case. …… In the opinion of this court, the conduct of the fourth respondent in attaching the bank accounts under section 44 in the facts and circumstances of the case was not warranted when the appeals preferred by the petitioner together with the stay applications were pending consideration before the first appellate authority. …………The impugned orders dated 17.7.2015, 9.6.2015 and 17.7.2015 (Annexure-E collectively to the petition) as well as the impugned orders dated 11.9.2015 Annexure-R-III collectively to the affidavit-in-reply of the respondent are hereby quashed and set aside. The third respondent Deputy Commissioner of Commercial Tax (Appeals) is directed to decide the stay applications filed by the petitioner within a period of fifteen days from the date of receipt of a copy of this order. Rule is made absolute accordingly with no order as to costs.

6. Not long ago, the High Court of Madras vide its judgment dt.05.06.2015 in the case of EDELWEISS COMMODITIES SERVICES LTD Vs COMMERCIAL TAX OFFICER held that “the respondent ought not to have rushed to issue the impugned notice when the revision petition is pending along with the stay application. In view of the same, the reivsional authority is hereby directed to take up the pending revision petition along with the stay application, and dispose of the same on merits and in accordance with law, within a period of four weeks from the date of receipt of a copy of this Order. It is made clear that till such time, the impugned orders shall be kept in abeyance. The writ petition is disposed of accordingly. No costs. Connected miscellaneous petition is closed”.7. Copies of the judgements are attached herewith, which can be quoted by the trade and industry while representing their case.

8. Even though various High Courts have directed the VAT department in various States not to resort to attachment of bank accounts, pending stay petition before the appellate authorities, the practice of attachment of bank accounts to meet revenue targets is not dispensed with. In some of the cases, before the dealer approaches the High Court, amount is transferred by the banks to the department and thereby leaving the dealer remediless. Therefore, there is need for issue of circulars by the Commissioners of Commercial Taxes of all the States to the assessing authorities under their jurisdiction instructing them to desist with the practice of attaching bank accounts in a very routine manner, when the stay petition is pending before the appellate authorities. The instructions from the Commissioners are expected only on directions by the High Courts. Trade and Industry need to take up at the Commissioners level for necessary instructions to the assessing authority. At the same time, they should pray the High Courts through the advocates at the time of hearing of attachment cases, for issue of directions to the VAT department for executive instructions in general that would be applicable to all dealers, which would help in saving of lot of time and money of dealers and precious time of Court

Regards

KK Singh

Prop- KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email-kksirclasses@hotmail.com

Thursday, November 19, 2015

FINANCE & LAW TODAY: Clause 49 -Corporate Governance and Company Law Pr...

FINANCE & LAW TODAY: Clause 49 -Corporate Governance and Company Law Pr...: Corporate Governance refers to the set of system, principles and processes by which a company is governed. Corporate Governance is base...

Clause 49 -Corporate Governance and Company Law Provisions

Corporate Governance refers to the set of system, principles and processes by which a company is governed.

Corporate Governance is based on principles such as

-Conducting the business with all integrity & fairness,

– Being transparent with regard to all the transactions,

– making all necessary disclosures,

– Complying with applicable Law,

– Accountability & responsibility towers the stakeholder.

Clause 49 of “Listing agreement” deals with the complete guidelines for corporate governance. Following are the provisions, a company, must comply to implement effective corporate governance.

Corporate Governance-:

In order to comply with clause 49(1) a company must adhere with some following principles.

- Right of Shareholder- As shareholders are the ultimate owner of the company, the company should seek to protect and facilitate the exercise of right of shareholders. A company must always be transparent with its shareholders and shareholders should have all the rights regarding General Meeting such as information about meeting, participate, Vote and questioning in GM etc.

- Role of stakeholders- A company must take care of stakeholder’s right and encourage cooperation between company & stakeholders. Their rights can be by Mutual agreement or by Applicable law or statute.

- Disclosure & Transparency- It is the obligation on company to be transparent with its stakeholders by giving disclosures of all material matters on timely basis. Disclosure can be regarding financial position, Performance, ownership and Governance etc. Non disclosure of Material Matter is Strictly Prohibited.

- Responsibility of Board- Members of the Board should disclose their interest in company and in any individual transaction and contract. They should also maintain the rule of confidentiality. They should also perform their key function such as preparation of major action plan, corporate Strategy, execution of Board, and effective financial Performance.

Board of Directors-:

1. Composition of Board

- Optimum Combination of Executive & Non Executive Directors,

- Not less than 50% of the board should comprise Non-Executive Directors,

- At Least one Women Director,

- Where chairman is non executive Director as least 1/3rd of the board should comprise Independent Director, and if

- Chairman is executive director then ½ of the board should comprise Independent Director.

| Chairman | Executive Director | 1/3rd of Board shall be Independent Director |

| Chairman | Non-Executive Director | 1/2 of Board shall be Independent Director |

2. Independent Director

Independent director shall mean “Non-Executive Director” other than Nominee Director, and shall be person who in opinion of board possesses integrity, relevant expertise & knowledge.

An independent Director shall not be

- The promoter or relative of promoter of the company or its holding or subsidiary or associates company,

- A person who by himself or his relative have any pecuniary interest other than salary , directly or indirectly, with the company or its holding or subsidiary or associate company,

- A person neither himself nor his relative hold or has hold the position of KMP or Employee in the company or its holding or subsidiary or associates company, in any of three financial year immediately preceding the FY in which he is proposed to be appointed.

- A firm of

- Auditor,

- Company Secretary,

- Cost Auditors, of the company or its holding or subsidiary or associates company or any legal firm which has transaction or amount more than 10% of the gross turnover of such firm.

- Holds together with his relative 2% or more of voting power,

- A chief officer or director or any NPO whose 25% of receipts comes from that company and any of it’s promote or director of the company or its holding or subsidiary or Associates Company.

- A material supplier, service provider or customer, or a lessor or lessee of the company.

- A person not less than 21 years of age.

Rules related to Independent director

i. Limit on Membership of Director- A person cannot be Independent director

-In more than 7 Companies,

– If whole time director then maximum 3 companies.

ii. Maximum Tenure- Independent Director can hold office for a term up to five consecutive years, and eligible for re-appointment of one more term.

If he has served for more than 5 years as on 1.10.2014 then he shall be eligible for reappointment for one another term and shall be eligible for reappointment after the expiry of three years.

iii. Formal Letter for Appointment- A formal letter of appointment shall be given to independent director and, brief profile of him shall be publish on the website.

iv. Performance Evaluation – Nomination committee shall lay down & disclose the criteria for performance evaluation and it shall be done by all board members except whose evaluation is being done. The term of the director shall be decided as per the performance evaluation.

v. Separate meeting of Independent Director- All the independent directors shall have at least one meeting in a year to

– Review the performance of Non-Independent director,

– Performance of Chairperson,

– Effectiveness of Board

vi. Training- Company shall provide suitable training to Independent Director.

3. Non executive Director’s Compensation & Remuneration

- Compensation to non executive director shall be fixed by the board with previous approval of shareholders in GM.

- Resolution shall specify the maximum No. of stock option to Non Executive Director

- Independent director is not eligible for stock option.

4. Other Provision of Board & Committees

- Board shall meet at least 4 times a year with a maximum time gap between two meet shall not be more than 120 days

- A director shall not be

– A member in 10 committees,

– Chairman of 5 committee in which he is director - Periodic Review of Compliance of law & regulation by board

- Removal, Resignation & reappointment of Independent Director.

5. Code of Conduct

- Board shall lay down the code of conduct,

- Board members and senior management personnel are bound to comply with that,

- Provision or codes are as per New Companies Act, 2013

Every person is responsible for such act of omission which had occurred within his Knowledge.

6. Whistle Blower Policy

- A vigil Mechanism , for actual or Suspected fraud or unethical Behavior shall be placed,

- Adequate safe guard shall be provided against victimization who avail the mechanism,

- The details of this mechanism shall be placed on company’s website

Audit Committee:-

The audit committee is a committee of the board of directors responsible for oversight of the financial reporting process, selection of independent auditor, receipt of audit results from both internal & external auditors. The committee assists the board to fulfil its corporate governance and overseeing responsibilities in relation to an entity’s financial reporting, internal control system.

- Minimum 3 directors shall be the members of Audit Committee,

- 2/3rd shall be the Independent Director

- All the members shall be financially literate & at least one member must have expertise in accounts & finance field.

- Chairman shall be Independent Director and must be present at annual general meeting.

- Company secretary shall act as secretary of committee.

At least four meeting in a year shall be held by audit committee with maximum time gap between two meetings shall not be more than 120 days. Quorum shall either two members or 1/3rd members of the committee which shall be higher but at least two independent directors must be present.

Powers of Audit Committee

- To investigate any activity within its terms of reference,

- To seek information from any employee,

- To obtain outside or legal advice,

- To secure attendance of outsider with relevant expertise, if any

Role of Audit Committee

- Overseeing the Financial reporting and disclosure process,

- Monitoring choice of accounting policies and principles,

- Overseeing hiring, performance and independence of the external auditor

- Oversight of regulatory compliance , ethics & whistle blower’s hotline

- Monitoring the internal control process,

- Overseeing the performance of internal audit function,

- Discuss risk management policies etc.

Nomination & Remuneration Committee:-

Nomination & Remuneration Committee shall be constituted by company which shall comprise

- At least three director,

- All shall be non executive,

- Half of the members shall be Independent Director.

The role of the committee is to formulate the criteria for determining qualification, positive attributes and Independence of Directors, Recommendation of remuneration policy. The committee shall also formulate criteria for person in management who deserves to be a director.

Subsidiary Company:-

At least one independent director must be the director of Material Non Listed Subsidiary Company. Audit Committee shall review the financial performance of subsidiary in order to have a good control or view of subsidiary company. Board of Holding must review all significant transactions and arrangements between holding & subsidiary, all MATERIAL SUBSIDIARIES shall be disclose to stock exchange.

Material Subsidiary means

- 20% of consolidated net worth is invested in the subsidiary company,

- 20% of the consolidated income coming from subsidiary company.

Risk Management:-

A company shall lay down procedure to inform board members about risk management, assessment and minimization procedure. The board shall be responsible for framing, implementing & monitoring the management plan. Company shall also constitute risk management committees

Related Party Transactions:-

A related party transaction is

- Transfer of resources, services and obligations

- Between company & related party as sec. 2(76)

- Regardless of whether a price is charged.

Parties are considered to be related if one party has the ability to control the other party & exercise significant influence over other party.

Forms of Related Party

Related Party shall be

- As define under section 2(76) of companies act, 2013

- KMP or relative of KMP of the company of its holding or subsidiary or associate company,

- Joint venture

Other provisions regarding Related Party Transaction

Related party transaction considered material if

- Aggregate transaction in a previous year exceeds 5% of total annual turnover, or

- 20% of the net worth of the company as per last audited financial statement.

All related party transactions requires previous approval from audit committee & all material related party transaction shall require previous approval from shareholders.

Disclosure-:

For good corporate governance company should make all necessary disclosures. It is also a responsibility on management to make disclosures of all material matters which all stakeholders are suppose to know. Stakeholders like creditors and customers can not attend meetings so the disclosure is only way through which they can get information.

Disclosure can be of following matters

- Related party transaction which is material in nature and policies for dealing with related party,

- Any accounting treatment, different from normal treatment & reason thereof,

- Remuneration to directors, facilities, perquisites etc given to directors. Any contract & arrangement entered into with them,

- Management disclosure and analysis report on various matters such as industry structure & development, opportunities and threats, segment wise or product wise performance, outlook, risk concern, discussion on financial performance.

transaction in which directors have personal interest shall also be disclosed - In case of appointment of new or reappointment of director some information about it like brief resume of director, nature of expertise in specific area, no. of directorship in other companies

- If any director resigns then the resignation letter along with detailed reason shall be disclose on company’s website.

- Training imparted to independent director , vigil mechanism and remuneration policy shall be disclose in the annual report of the company

- When money rose through public issue, right issue, or preferential right, the company shall disclose their intended use & actual use, on quarterly basis.

A statement on annual basis shall also be prepared for the fund utilized for the purpose other than those for which they were being acquired.

CEO/CFO Certification-:

Any managing director, CFO or whole time finance director, who is in discharging of finance function, must certify to the board that the financial statements have been reviewed by him and present the true & fair view and do not contain any material untrue statement or misstatement.

He also indicate to auditor or audit committee if

- There is any material change in internal control system,

- Change in accounting policies,

- Knowledge of any fraudulent activity being noticed by them

Report on corporate governance-:

A company must give a separate section on Corporate Governance in annual report, where all the disclosures regarding compliance & non compliance with mandatory requirement and the extent to which non mandatory requirements have been adopted.

Quarterly compliance report shall be given to stock exchange within 15 days from the date of closure.

Compliance- Company shall obtain Annual Activity Certificate from auditor or practicing company secretary, about the compliance of the clause 49 of Listing Agreement.

Conclusion-:

The main motive of this clause is that company should be fair with its stakeholders. Everything in the company must be done effectively & fairly. Since the Stakeholders have social & financial interest in the company hence company is bound to provide a safeguard to their interest.

Regards

KK Singh

Prop- KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email- kksirclasses@hotmail.com,advocatekksingh@outlook.com

Monday, November 16, 2015

FINANCE & LAW TODAY: 11 Tips to build your wealth which no advisor will...

FINANCE & LAW TODAY: 11 Tips to build your wealth which no advisor will...: India is amongst the country where people know the value of savings. We save a lot in comparison of other countries. Still when it comes ...

11 Tips to build your wealth which no advisor will tell you

India is amongst the country where people know the value of savings. We save a lot in comparison of other countries. Still when it comes to possess wealth we stand far behind. Earning, saving and wealth creation these are three different aspects of meeting our financial goals. Now question is what should be our financial goal. How we should decide that this particular level is our financial goal. Let us help you hear to decide and achieve that goal.

1) Wealth building is not equal to accumulation of money but to create new sources of income without any future action from your side: Well we have different concepts for financial security but in real world financial security means for what period of time you can manage your current lifestyle if you stop working right now. Achieving this level should be the goal of your wealth building.

2) Start buying income generating resources: Now you can understand. Wealth creation doesn’t mean to accumulate money but to create sources which can fetch you return when you don’t even interfere in their natural movement. For every expanse you make or will have to make to manage current lifestyle there must be an asset, here asset means a source which can fetch you earnings to meet those expanses.

Robert Kiyoski in his famous book ‘Rich dad Poor dad” makes it very simple that an asses is simply a resource which is going to fetch some cash flows in future.

3) Start from small savings: Always start from small savings. Generally we save after meeting our expanses but to maintain a strict discipline we should save first and then make out budget to meet all expanses in available sum.

4) Invest in real asset: In early stage of life we should try to accumulate these real assets which are going to fetch some risk free returns. Like stocks of good quality, Fix interest rate debentures, Tax free Bonds, Liquid funds with dividend option. Once you accumulate a decent sum you can put it in real estate options and can fetch some rent income and capital gains.

5) Hedge your investments with hedging products: What are these products? In case you have a heavy investment mutual funds and after that market is up and you are expecting it to go even higher but still confused because if it came down you will miss an opportunity to book decent profits. You can hedge this situation by buying put options representing the portfolio you have in your account. Likewise you can hedge all investments through some counter or opposite investments where the reaction of movement is sharper.6) Be less excited: It may sound a little surprising but more excitement is dangerous for your investments. In equity market there will sharp movements every day in some scrip. Don’t get carried away with that. Most of the people making huge losses in market only because of this excitement of catching the sharp movements. Wealth is a long term phenomena and you can’t tame market ever.

7) Emotional control: What emotion will do with this wealth creation thing? Emotion is not only about love or friendship. It also includes our greed and laziness which force us to take unwise decision. I have seen many people suffer a loss and then they continue to suffer more losses just to recover that first one. Emotion attached with lost money never let them leave the speculation and they lose even more.

8) Profit is all about entry at low and exit at high: Correct timing is very important aspect of wealth building either you will suffer loss in every investment. But in real word people rely on past trends and are not ready to put any money in the fund or scrip which is at low level and they are unable to see huge profit in past returns.

9) Don’t expect past trends to repeat every time: Products rarely repeat their past trends. Take the latest example, return of last year for equity was almost 100% but in current year market is stagnant. While choosing your fund it is better to see past trend of longer period and read it with current scenario and decide with future expectation.

10) Control your greed: If you are earning in any investment, just book it don’t wait for a miracle. If you are losing hold and average.

11) Don’t go after tips: It’s the worst investment to buy any tips from so called experts. If someone is so sure of market they can put their own money. You will end up in losing a chunk of money. Keep patience and go for long term investments. Review your investments time to time and make changes according to changes in economy and long term trends. Never forget to take the services of professional advisor.

Let me sum up some basic rules for you

No risk no gain…high risk high gain but it may result in loss of your entire capital too

No one ever become a millionaire by speculation in shares. There are some fake stories in market, don’t get carried away by them

In case you make any loss. Forget it and leave don’t try again and again to recover your loss. It will result in more losses.

Give time some time. A correct timing is the most important aspect of investing.

Be consistent and disciplined in investment. SIP is one of the best products to keep discipline and consistency.

Try to start some SIP’s which will be deducted within one week of your date of credit of salary in account.

This way you will be able to save first and control expanses

Keep your time horizon at least one year for equity based products and for less a year time go with fixed income products

Regards

KK Singh

Prop- KK Sir's Classes

wwwkksir.blogspot.in

wwwkksingh.blogspot.in

Email- kksirclasses@hotmail.com,advocatekksingh@outlook.com

Subscribe to:

Comments (Atom)